Ever since the fall of the Berlin wall in 1989, Western policy has been guided by two underlying beliefs: that the world would become ‘flat’; and that its states would ultimately adopt the institutional, economic and value systems of the West. For many years, these beliefs served as the north star for policy-makers’ decisions and formed the basis for businesses’ global strategies. However, at some point during the last decade, this north star started to look increasingly at odds with the actual state and direction of the world. Barriers have been on the rise, and western-led order in retreat. And yet, no new navigational chart, let alone north star, has so far emerged to point us in a clear direction. Looking at the bigger US-EU-China dynamics at play, this is our sketch of such a chart.

The tectonic shift of power from West to East is reaching a critical juncture. It is the force that connects all specific issues shaping current global relations. China’s growth story is historically unprecedented in both scope and speed. Since the global financial crisis in 2008, while the West has grappled with low growth, China’s economy has tripled in size. And COVID is now acting as a great accelerator for China’s relative rise, putting it on fast-track to overtake the US as the world’s largest economy by the end of this decade.1

It is not only a question of size – it is also one of quality. While Silicon Valley won the first round of digitalization, Shenzhen won the second. And China is doubling down in its ambition to lead in the key technology areas of the next decade – AI, biotech, neuroscience, quantum communications, cleantech.

In response to this, both the US and the EU are in defence mode, trying to do two things simultaneously: aligning their own relationship and positioning, while seeking to define a common strategy towards China. Both are coming from very different starting points, however: the US has been on course for a decoupling from China, while the EU has retained a more open approach, as shown by the recently signed investment agreement with China, which favours a recoupling.

China has already put its strategy for the upcoming years in place (dubbed ‘dual circulation’). By increasing its share/autonomy in high-value products (e.g. telco/5G, pharma, biotech, aerospace), China seeks to rebalance towards domestic consumption, drive productivity growth, and reduce its dependence on critical imports like semiconductors, given the “complicated international situation”.

However, it would be wrong to read into this a retreat from global markets, as the strategy also spells out a further opening up, which reflects China’s interest in raising productivity through exposure to international competition and a shift to a market-based pricing of credit risks – in other words, moving towards a market economy. Recent policy changes lifting foreign ownership restrictions indicate the significant dynamics underway in spite of global tensions: While global FDI collapsed in 2020, China hit a new record with inflows of USD163bn, overtaking the US as the world’s largest FDI recipient.2 And with foreign holdings of Chinese onshore financial assets at nearly 1 trillion USD (Q3/20)3, China’s equities and bond markets are now the second-largest worldwide, with US investors emerging as key drivers of this trend. The new EU-China investment agreement is set to further reduce investment restrictions, boosting the EU’s hitherto modest investments into China.

Meanwhile, the West is moving in the opposite direction: After years in which free trade and market efficiency were the key principles driving economic policy, the US and Europe have shifted to an activist economic policy agenda. Whether the increasingly restrictive FDI regulations and decisions, strengthened buy-local provisions, or the industrial policy design of economic recovery programs, we are clearly seeing a new zeitgeist, that depending on one’s standpoint, reflects a page from the playbook of successful risers like South Korea, Singapore, and China, and at worst a retreat to protectionist policies4 fuelled by populism and at times even outright xenophobia5.

Where does this leave us? As it stands it seems that coming from two different ends of a spectrum, the West and the East are converging towards what can be described best as a two-circle world: an inner circle of re-emphasized autonomy, marked by a more activist industrial policy around national security and strategic interests; and an outer circle of continued globalization and potential cooperation on global challenges. The billion-dollar question is which topics will be restricted to the inner circle, and which topics could be included in the outer circle. If the intersection remains limited to “defence topics” such as terrorism, nuclear-strategy, climate, and energy, the world will move towards an increasingly decoupled world, which would also raise the spectre for conflict. If, however, the West and China agree to put “offense topics” such as global standards on 5G, AI, and biotech in the intersection, there is potential for a recoupled world.

China sees itself at a moment of opportunity, having come out of COVID on top and seeing Western democracies on the defence. President Xi used his speech in Davos to make China’s position on the next chapter of globalisation crystal-clear: he used “decoupling” and “new cold war” as synonyms. China will be open to cooperation. But it is no longer willing to subordinate. Assimilation, the idea that China would integrate into the Western-led order, is a non-starter for China. This new self-confidence finds its expression in the name of the new diplomatic strategy of “bridging”. This will become crucial as at the same time more and more leaders in the West consider western values and human rights as a kind of minimum requirement for future cooperation. And were the West to move towards decoupling, China will accelerate its efforts to compete on all levels and defend its interest by strength – its recent military exercises across the Taiwan Strait must be understood as a warning.

The US political and public discourse on China is certainly not promising. Calls for containment and cold-war strategies have become the mainstream and the Trump administration’s hawkishness on China is almost considered as the minimum threshold in the evaluation of the incoming administration’s China policy. In contrast to Europe, the economic relationship is politically perceived as a liability.6 However, rather than a strategy, such approach would be a self-fulfilling prophecy.7 The good news is that President Biden has a deep grasp of the complexity of the challenge posed by China’s rise. China is too big and impactful to be isolated or contained, which means that the relationship needs to be managed and issues compartmentalized to allow for cooperation where possible, even at times of heightened tensions. Biden and his administration will take some time to define their strategy towards China.8 One key element is already clear: Biden wants to bring the world’s major democracies and US allies – the EU, UK, Japan, Australia and India – on board to create leverage.

To do so, however, will require openness to alternatives to the hardcore decoupling strategy initiated by Trump. Europe is the smallest of the three big powers. Yet, by sitting between East and West, Europe plays a critical role. Europe’s leaders are enthused about the prospect of a transatlantic realignment under President Biden, but at the same time, Europe made a conscious decision to take decisions on the basis of its own interests. Regarding China, Europe’s position is ambivalent: EU Commission President Von der Leyen views China primarily as a ‘strategic competitor’, German Chancellor Merkel continues to believe that China ultimately must be a ‘partner’. The fact that Europe is about to enter a critical transition period, with Europe’s geopolitical heavyweight Merkel stepping down at the end of the year and French President Macron facing a tough re-election challenge in Spring 2022 means the EU need to find answers on its future positioning, its partnership with the US, and its relationship with China on a sprint.

Embracing China or fighting against it. These are the two extremes. Whether or not the leaders decide on decoupling will become the biggest question of this decade. We believe there are reasons for guarded optimism for a hybrid with upside potential. Cooperation at least on global challenges. Coordination on global standards. Competition on innovation. If China continues its market liberalization, there is scope for progress on the economic side. Even on the protracted issue of security there are ways to square the circle: A draft law of the German Government on IT-Security contains a potential global solution: instead of banning players from China, a “trustworthiness-check” is one part of a comprehensive security architecture. A second part is that every business partner of a Chinese vendor would be responsible for compliance at the intersection of both companies. Similar to ESG standards, responsibility is interpreted beyond the P&L. The intersection of the West with China as well as the intersection of business partners will trigger the next chapter of globalization.

Global Perspectives and Expectations: Expert Views from Across the World

USA: The Biden administration will continue President Trump’s tough stance on China, although with more nuance and predictability in policy making. For Western corporates, this means continued scrutiny on Chinese operations, technology, investments and M&A that are either based in China or linked to China-owned companies. It is more important than ever for Chinese corporates to build trust based on facts and transparency.

China: The credibility of the U.S. model has suffered abroad, and especially in China. Western companies will increasingly need to navigate nationalistic sentiment in China, while avoiding sounding sanctimonious about Western values and business models.

Japan: will look to benefit from evolving US-China relations, not only politically but also economically – especially in winning infrastructure work in ASEAN.

UK: After attempting a cautious but co-operative relationship with Beijing, the UK Government has been driven by events towards a more hawkish stance. Concern over the treatment of the Uyghur people, along with changes in the position of Beijing towards Hong Kong, seen to have violated Sino-British joint declaration, have brought a distinct chill to the UK-China relationship. The UK policy response has been notable, with Huawei restricted from expansion into UK 5G, a new FDI screening process driven largely by concerns over Chinese investment, and sanctions for UK businesses with supply chains exposed to labour abuses in Xinjiang. Of most concern is that the UK does not appear to have a coherent strategic policy response to the rise of China to global superpower status, but rather a patchwork of individual responses to individual events.

EU: The EU’s relationship to China will continue to be characterised by ambivalence with areas of cooperation (climate change, global stability), competition (strategic industries), and conflicting values. EU business interests and an understanding of China’s growing global importance will continue to provide a counter current against decoupling. Chancellor Merkel pushed hard for more cooperation with China. Soon, it will be up to others to make a call whether to continue or to change this strategy.

Middle East: The GCC will continue to balance its relations between Beijing and the West, selling China its energy and enjoying bilateral infrastructure deals under the Belt Road Initiative, whilst Western commercial interests will remain central in driving the region’s attempts at economic diversification away from oil under a Western security umbrella.

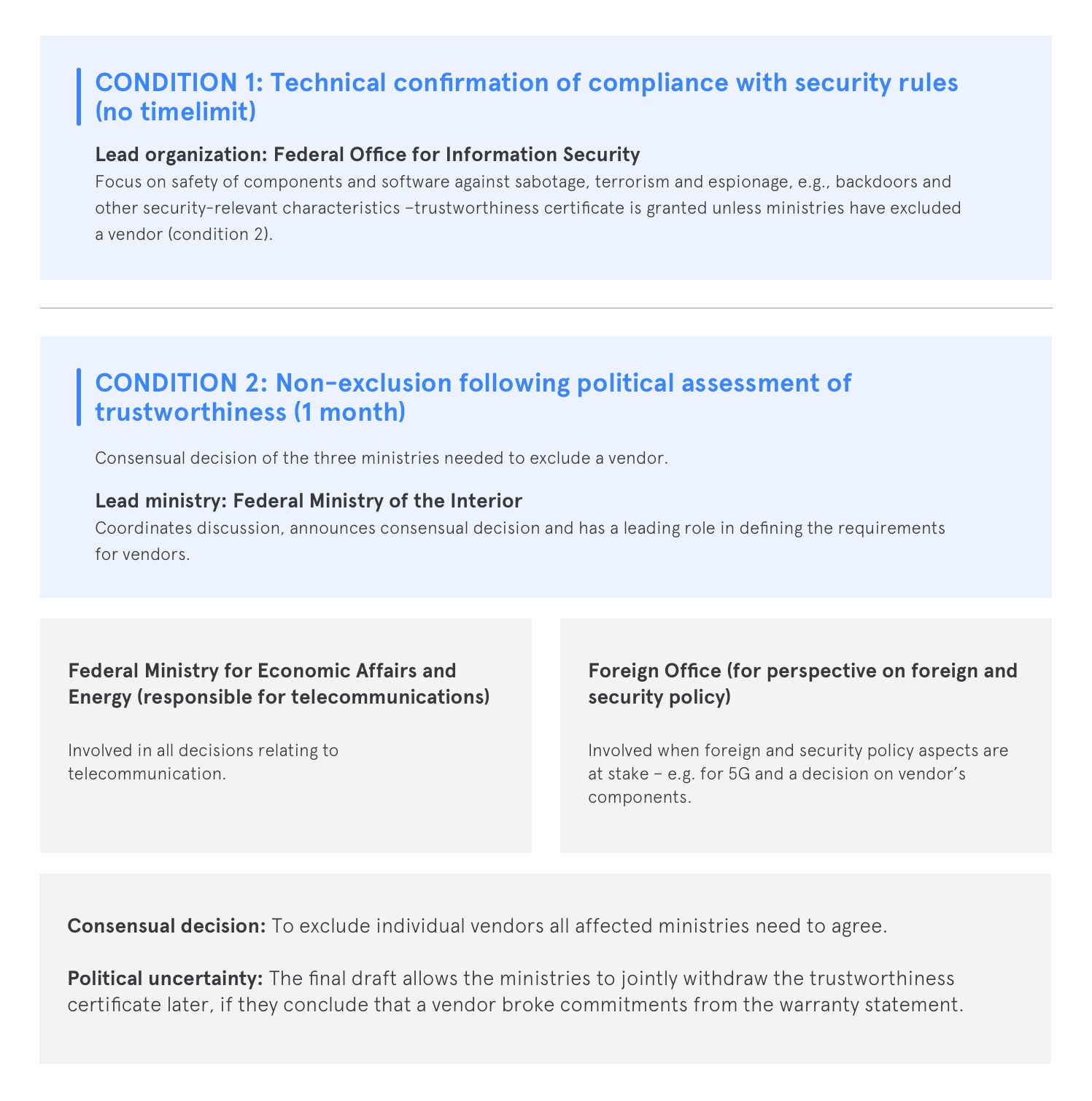

Assessment: Certification Of 5G Suppliers In Germany

First step:

Telecom operator notifies Federal Ministry of the Interior of intention to use critical components (as defined by Federal Office for Information Security) and provides the vendors warranty statement for trustworthiness (content defined by Federal Ministry of the Interior, also covering security concerns and assurances e.g. on risks arising from foreign „legal obligations“).

Two conditions to receive trustworthiness certification:

Lead Authors:

Joachim Koschnicke, Partner, Berlin

Matthis Kaiser, Managing Director, Berlin

Co-Creators / Contact:

Brett O’Brien (Managing Director, Washington, DC)

Victoria Esser (Managing Director, Washington, DC)

Jack Krumholtz (Managing Director, Washington, DC)

Paul Yang (Partner, Beijing)

Claudia Kosser (Managing Director, Shanghai)

Mei Zhang (Managing Director, Hong Kong)

Minako Hattori (Partner Tokyo)

Faeth Birch (CEO UK and International)

John Gray (Partner, London)

Henriette Peucker (Partner, Brussels)

Cornelia Quennet-Thielen (Senior Advisor, Berlin)

Dirk von Manikowsky (Partner, Dusseldorf)

Jeferson Brito Andrade (Senior Design Consultant, Berlin)

Sönke Hillebrandt (Associate Director, Berlin)

Philip Steinbrecher (Senior Associate, Brussels)

Katinka Ringlstetter (Associate, Berlin)

Kim Kea Schulte (Associate, Dusseldorf)

Simon Moyse (Managing Partner, Dubai/Abu Dhabi/Riyadh)

1https://fortune.com/2021/01/18/chinas-2020-gdp-world-no-1-economy-us/

2https://www.reuters.com/article/us-china-economy-fdi-idUSKBN29T0TC

3https://www.piie.com/sites/default/files/documents/pb20-17.pdf

4https://www.economist.com/leaders/2021/01/30/buy-american-is-an-economic-policy-mistake

5https://www.bloomberg.com/opinion/articles/2020-09-06/u-s-ban-of-chinese-students-takes-things-to-extremes?sref=e9953brd.

6https://economics.mit.edu/files/11499

7https://www.ft.com/content/83a521c0-6abb-4efa-be48-89ecb52c8d01

8https://www.wsj.com/articles/bidens-china-policy-to-be-steered-by-team-of-rivals-11612348201